Mobile AR: Usage and Consumer Attitudes, Wave I

Mobile AR: Who’s Using it? When? And How?

ARtillry’s latest intelligence briefing examines original survey data. Preview the report, or subscribe.

Executive Summary

How do consumers feel about mobile AR? Who’s using it? How often? And what do they want to see next? Perhaps more importantly, what are non-users’ reasons for disinterest? And how can app developers and anyone else building mobile AR apps optimize product strategies accordingly?

These are the questions we set out to answer. Working closely with Thrive Analytics, ARtillry Intelligence wrote questions to be presented to more than 2000 U.S. adults in Thrive’s established consumer survey engine. The results are in and we’ve analyzed the takeaways in a narrative report.

This follows last month’s ARtillry Intelligence Briefing, which examined mobile AR app strategies and business models. Now, a deeper view into real consumer usage and attitudes validates those findings, while providing new dimension on mobile AR strategy development and opportunity spotting.

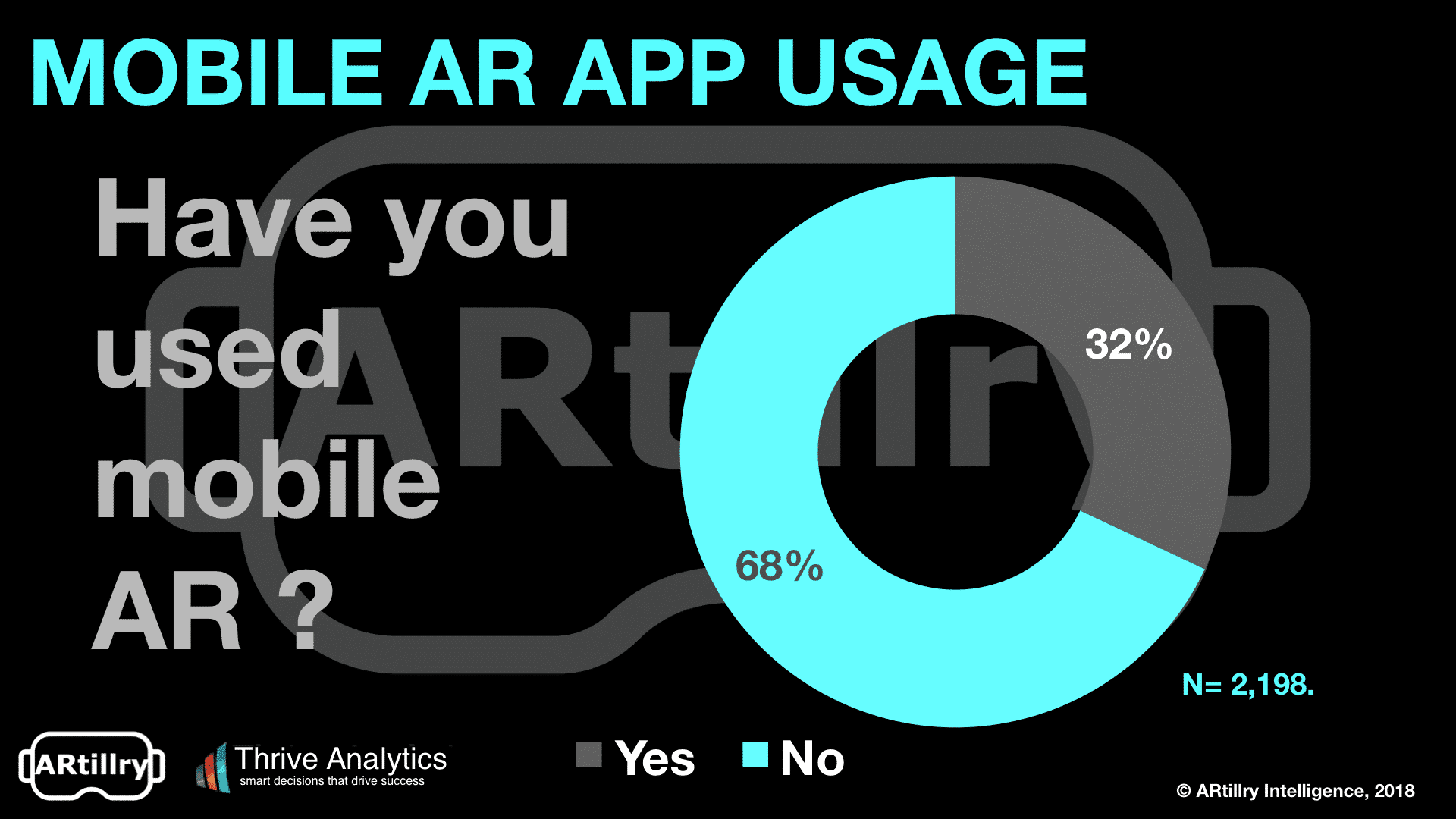

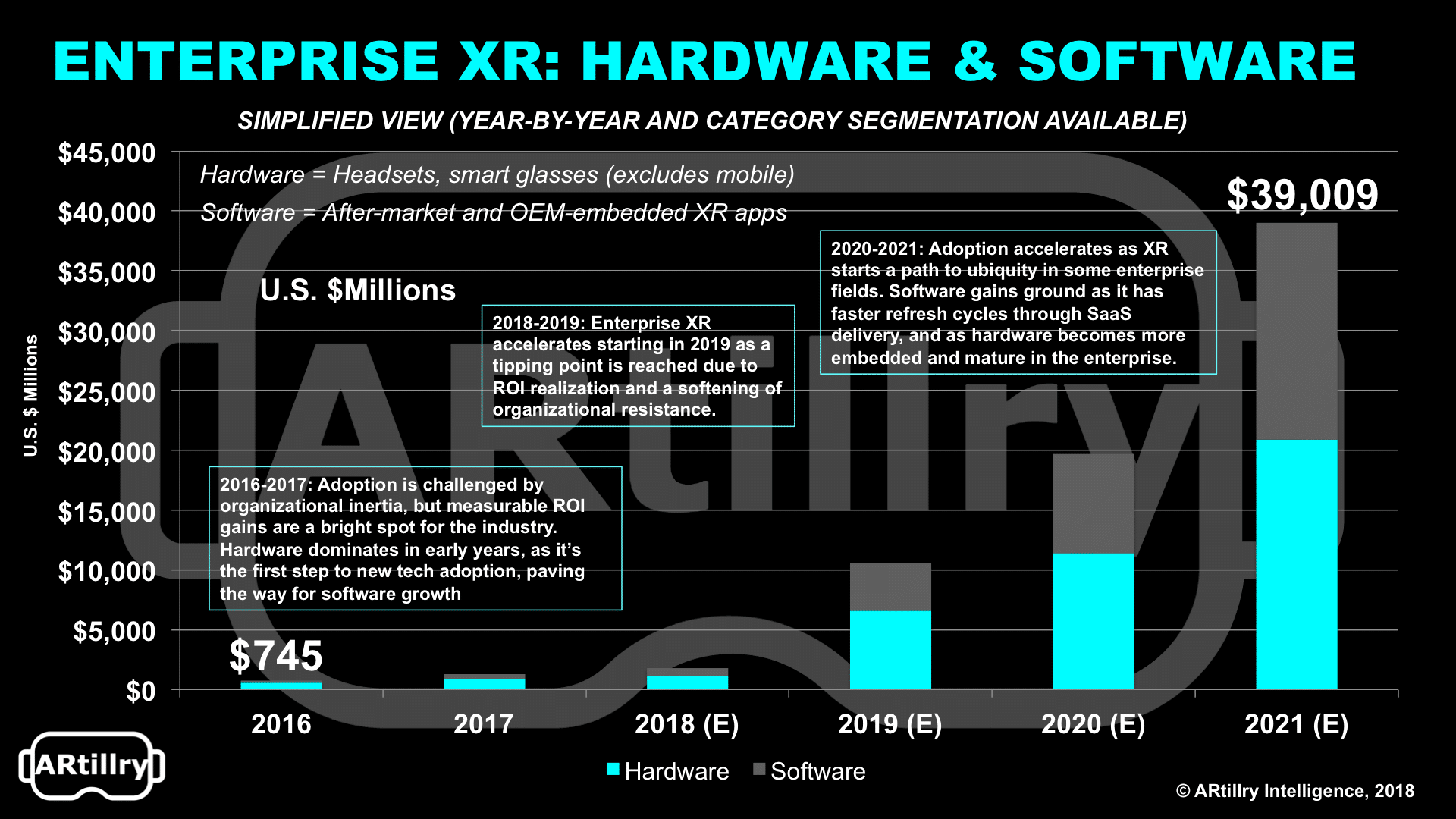

As for the findings, one third of consumers surveyed have used a mobile AR app. And those consumers appear active and engaged, with more than half reporting that they use mobile AR apps at least weekly. The top app category by far is gaming, which we attribute to Pokémon Go’s popularity.

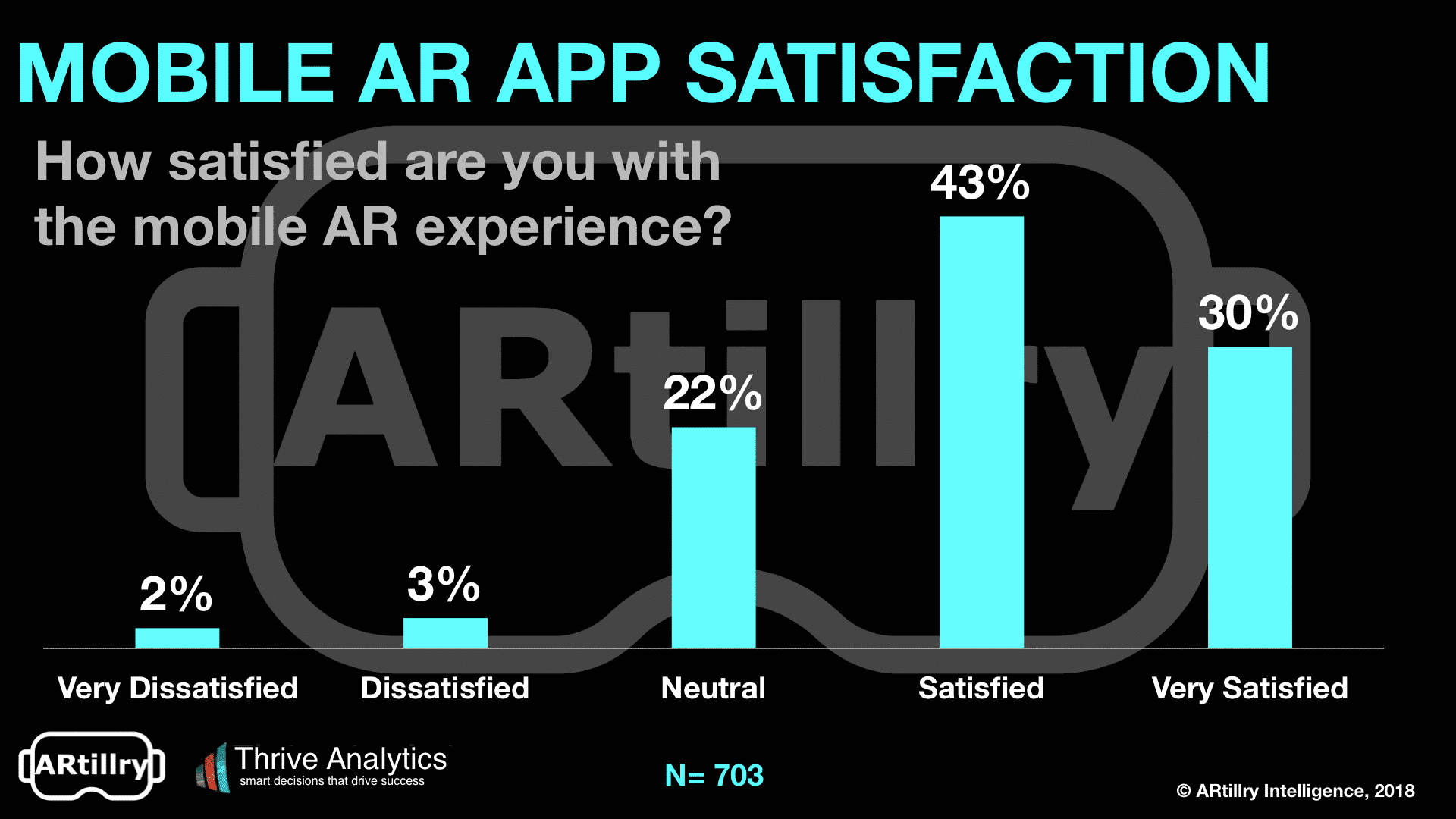

Mobile AR users are also engaged, with 73 percent reporting satisfaction or high satisfaction. But beyond these and a few other positive signals, there are some negative signs and areas for improvement. For example, non-mobile AR users report low likelihood of adopting soon, and an explicit lack of interest.

This disparity between current-user satisfaction and non-user disinterest underscores a key challenge for immersive technologies: you have to “see it to believe it.” In order to reach high satisfaction levels, apps have to first be tried. This presents marketing and logistical challenges to push that first taste.

Put another way, AR’s highly visual and immersive format is a double-edged sword. It can create strong affinities and high engagement levels. But the visceral nature of its experience can’t be communicated to prospective users with traditional marketing such as ad copy or even video.

The same challenge was uncovered in our corresponding VR report last August (we’ll publish the second wave in Q3). This makes it a common challenge with immersive media like AR and VR. It will take time and cost reductions before they reach a more meaningful share of the consumer public.

Meanwhile, there are strategies to accelerate that process, and to build AR apps that are compelling to consumers’ current standards. In the coming pages, we’ll examine those strategies and unpack the rest of the survey findings. This is meant to empower readers with a greater knowledge position.

Table of Contents

Introduction: A Snapshot

In last month’s ARtillry Intelligence Briefing, we examined mobile AR app strategies and business models. This compelled us to follow up with additional dimension into AR strategies. And the best way to do that is to ask consumers how they feel. So we fielded the latest AR consumer survey.

In last month’s ARtillry Intelligence Briefing, we examined mobile AR app strategies and business models. This compelled us to follow up with additional dimension into AR strategies. And the best way to do that is to ask consumers how they feel. So we fielded the latest AR consumer survey.

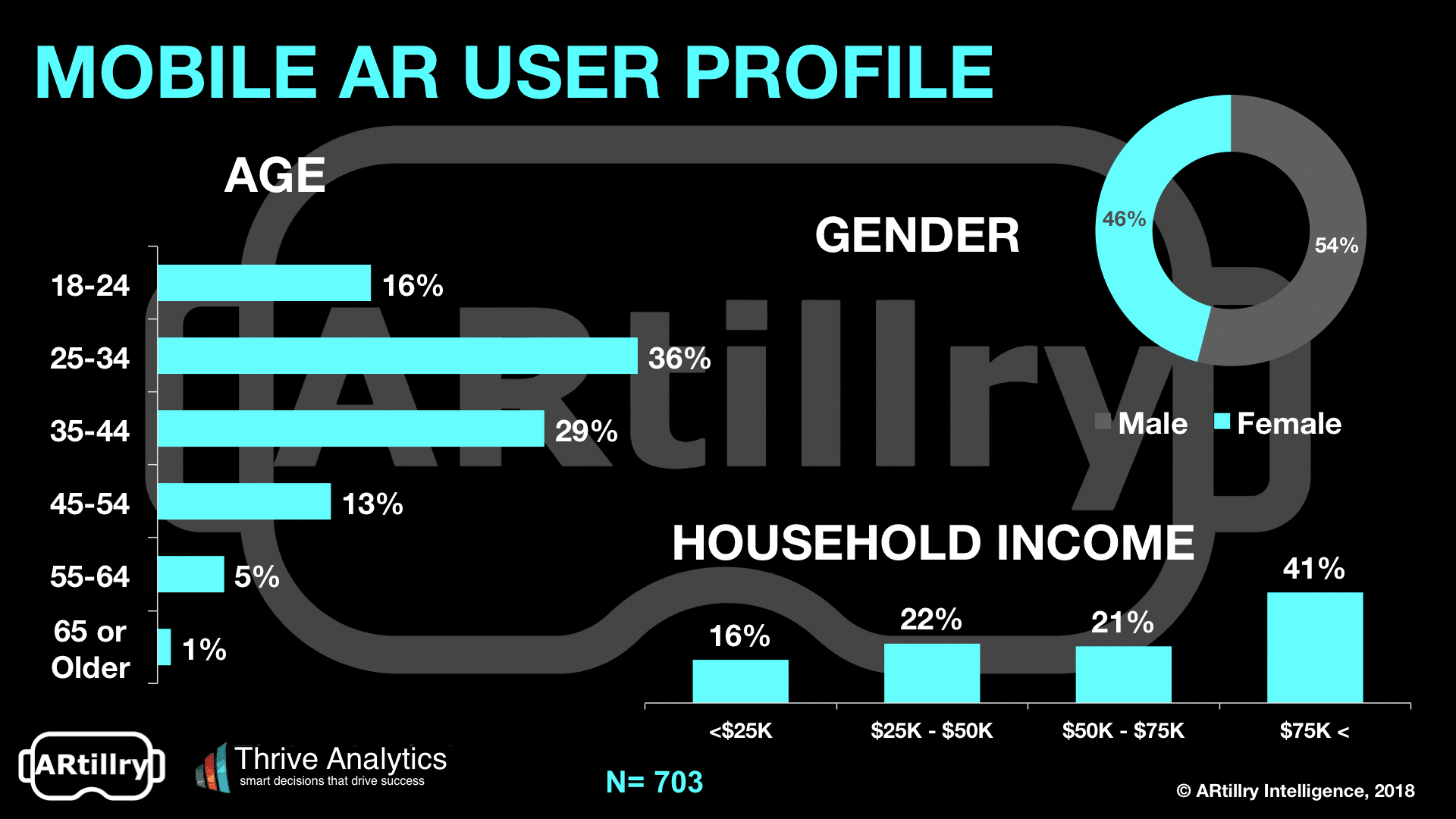

Working closely with our data partner Thrive Analytics, ARtillry Intelligence wrote questions to present to a sample of more than 2000 U.S. adults. This represents the second wave of Thrive’s Virtual Reality Monitor. And now that the results are in, there are several implications and takeaways.

The survey results are a telling snapshot of mobile AR adoption, which we’ll detail in the coming pages. That will include charts and a narrative story arc that unpacks strategic takeaways, and our outlook for mobile AR. But before we take a deeper dive, here are a few of the questions we’ll answer.

— 32% of consumers have tried mobile AR.

— 73% of mobile AR users are either satisfied or very satisfied.

— *% of mobile AR users are active monthly, *% are active weekly.

— *% of mobile AR users have used games, *% have used social apps.

— *% of mobile AR users want more games, *% want education apps and *% want city guides.

— *% of mobile AR users would pay $1.00 or more for an app, *% would pay $5.00 or more.

— *% of non-mobile AR users are unwilling to pay any amount for mobile AR.

— *% of non-mobile AR users are unlikely or extremely unlikely to try mobile AR.

— *% of non-mobile AR users don’t know where to look for apps, or if their phone is compatible.

*Subscribe to see the full data set.

Video Companion

Methodology

ARtillry Intelligence has partnered with Thrive Analytics by writing the questions for the Virtual Reality Monitor consumer survey. These questions were fielded to 2,198 U.S. Adults. Additionally, ARtillry Intelligence wrote this report, which contains its own insights and viewpoints on the survey results.

For any market sizing, ARtillry Intelligence follows disciplined best practices in market sizing and forecasting, developed and reinforced through its principles’ 15 years in research and intelligence in the tech sector. This includes the past 2.5 years covering AR & VR exclusively, as seen in research reports and daily reporting.

Thrive Analytics likewise follows best practices in consumer research, developed over its long tenure as a consumer research firm. More information and background on each firm can be seen at the above links and ARtillry’s disclosure and ethics statement is below.

Disclosure and Ethics Statement

ARtillry has no financial stake in the companies mentioned in this report, nor received payment for its production. With respect to market sizing, ARtillry remains independent of players and practitioners in the sectors it covers. It doesn’t perform paid services or consulting for such companies, thus mitigating bias — real or perceived — in market sizing and industry revenue projections. Disclosure and ethics policy can be seen in full here.

Preview the report, or subscribe to access it in full.

{kind=link}