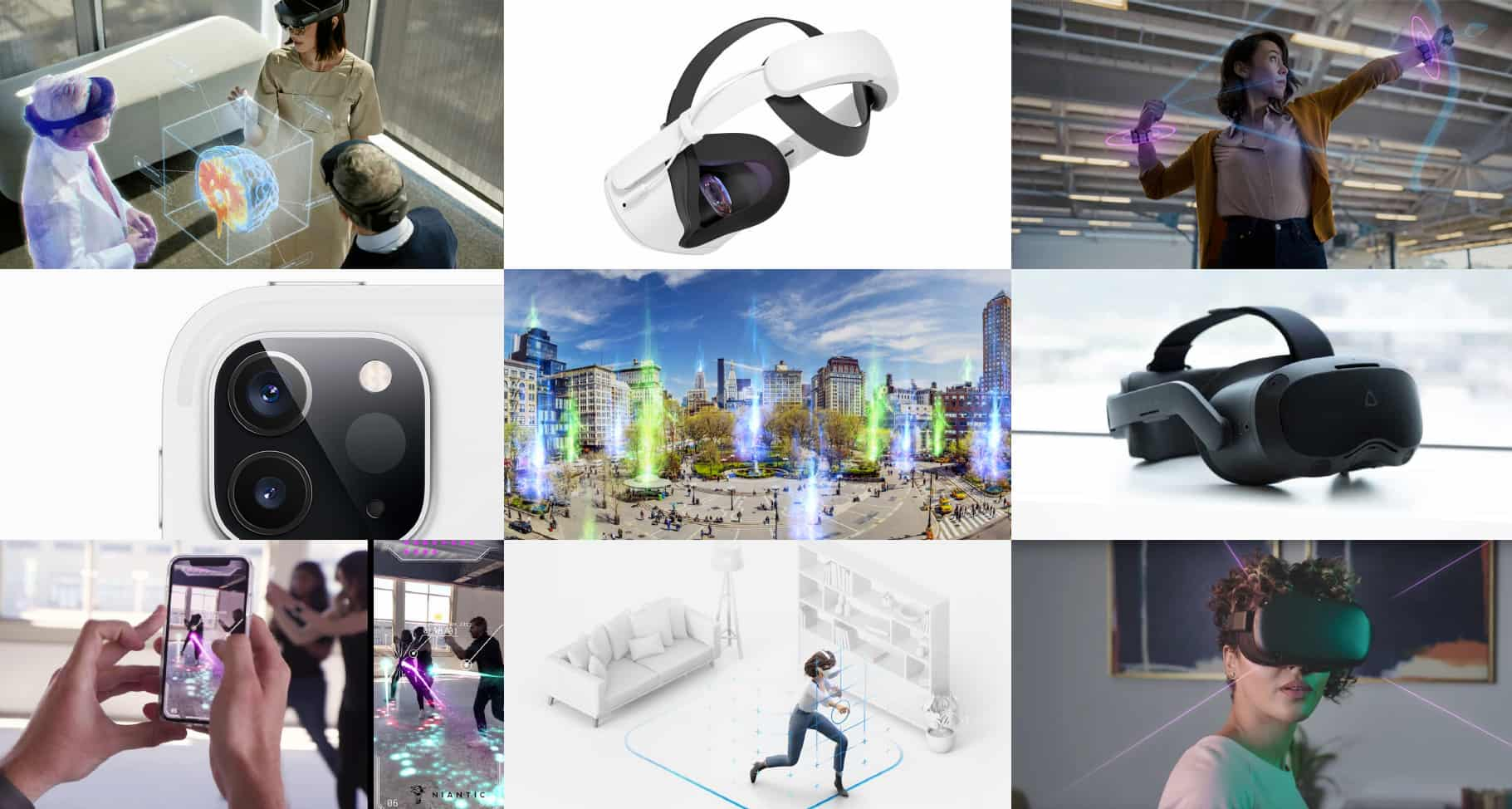

AR and VR – collectively known as spatial computing – continue to hold immense potential. Though they don’t represent the imminent tech revolution trumpeted in their circa-2017 hype cycle, they continue to show gradual progress. After a shakeout followed that hype cycle, AR and VR are now steadily growing at measured and realistic paces.

But the spatial spectrum deserves more nuanced analysis as there are varying growth curves across AR and VR subsectors. Those seeing the most commercial traction include AR marketing & commerce, and consumer VR. Meta (formerly Facebook) continues to advance the latter with massive investments and loss-leader pricing for its flagship Quest 2.

Speaking of Meta, one thing that characterizes spatial computing in 2021 – for better or worse – is metaverse mania. The term resurfaced in 2021 after several mini-hype cycles over the past 30 years. This time, the volume was amplified as the metaverse aligns with growth in AR and VR noted above… not to mention Meta’s highly-exposed investments. It spends $10 billion+ annually to accelerate its vision.

But as this metaverse hype cycle accelerates, there are mixed feelings among AR and VR proponents. On one hand, it brings unprecedented exposure to their work, which translates to investor and consumer excitement. On the other hand, connection to the “m-word” clouds AR and VR in mainstream perception as being futuristic jargon.

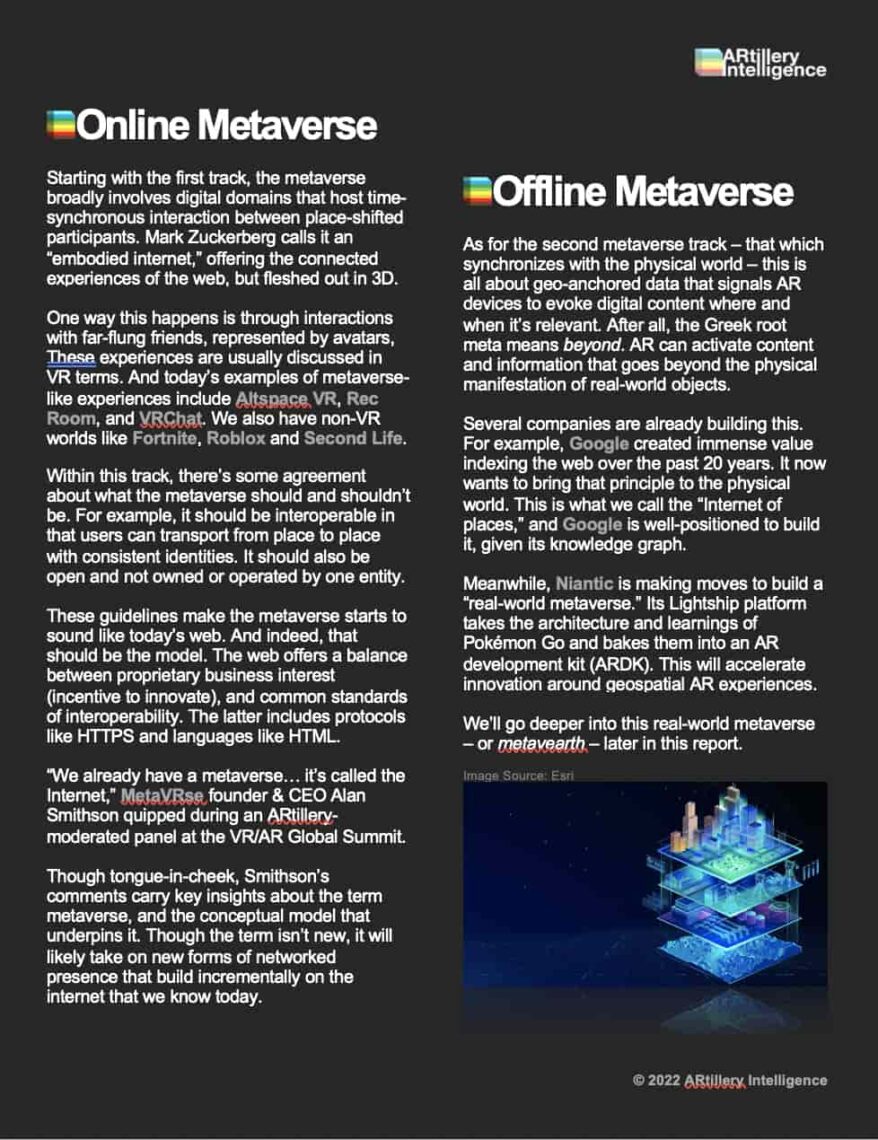

Stepping back, what is the metaverse? Mark Zuckerburg calls it an “embodied internet.” In other words, you’re in the internet instead of on the internet. This manifests in 3D virtual spaces that host time-synchronized interaction between place-shifted participants. Today’s metaverse-like fiefdoms include multiplayer games like Fortnite and Roblox.

But it’s not just about 3D gaming. The metaverse has two tracks. One is fully-immersive, mostly in a VR context. The other is a physical-world metaverse, where geo-anchored data triggers AR devices to evoke digital content where and when it’s relevant.

The second metaverse track involves a multi-dimensional data mesh that enables geo-relevant AR experiences. Think of this as an annotation layer for the world or an Internet of places. We refer to this as the metavearth, and a similar construct is known in spatial computing circles as the AR cloud.

Beyond Meta, others are investing in versions of the metaverse, including Google, Apple, Microsoft, and Niantic. They’re each driven to protect and future-proof core businesses. But a by-product of these self-interested investments will be an accelerated AR ecosystem. And acceleration is needed for a key step: the transition from mobile to head-worn AR.

So where are we in that journey? What did we learn in 2021? And what’s to come in 2022 across the subsegments of the spatial spectrum? We dive into these questions and others through numbers, narratives, and concrete predictions. The goal, as always, is to empower you with a knowledge edge.

The fastest and most cost-efficient way to get access to this report is by subscribing to ARtillery PRO. You can also purchase it a la carte.

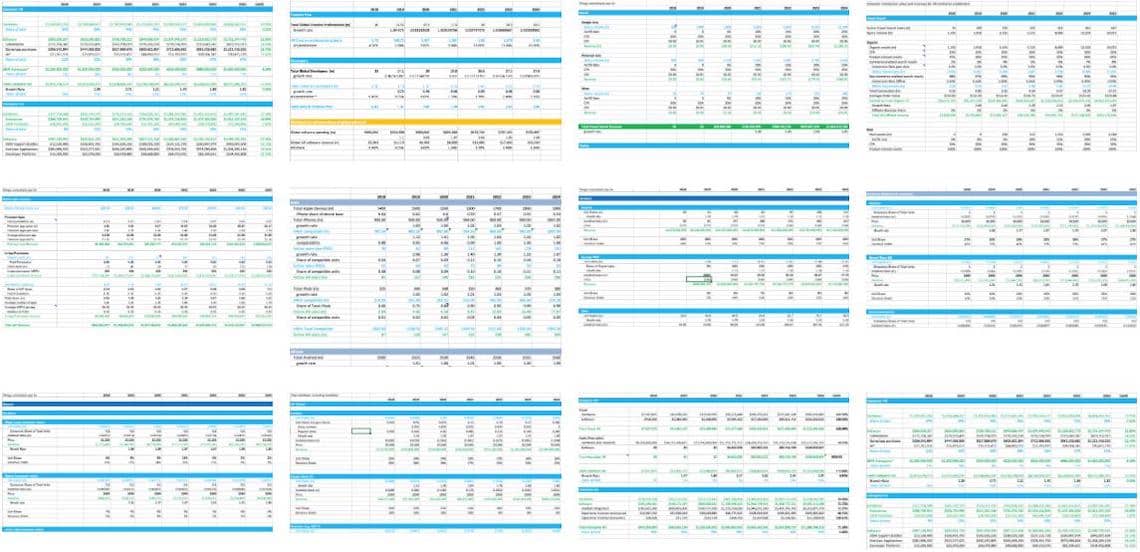

This report highlights ARtillery Intelligence’s viewpoints, gathered from its daily in-depth coverage of spatial computing. To support the narrative, data are cited throughout the report. These include ARtillery Intelligence’s original data, as well as that of third parties. Data sources are attributed in each case.

For market sizing and forecasting, ARtillery Intelligence follows disciplined best practices, developed and reinforced through its principles’ 15 years in tech sector research and intelligence. This includes the past 4 years covering AR & VR exclusively, as seen in research reports and daily reporting.

Furthermore, devising these figures involves the “bottom-up” market-sizing methodology, which involves granular ad revenue dynamics such as campaign pricing and spending. More about ARtillery Intelligence methodology can be seen here, and market-sizing credentials can be seen here.

Unless specified in its stock ownership disclosures, ARtillery Intelligence has no financial stake in the companies mentioned in its reports. The production of this report likewise wasn’t commissioned. With all market sizing, ARtillery Intelligence remains independent of players and practitioners in the sectors it covers, thus mitigating bias in industry revenue calculations and projections. ARtillery Intelligence’s disclosures, stock ownership and ethics policy can be seen in full here.

Checkout easily and securely.

Ask us anything

Credentials & context